When I moved to Finland in September 2021 I had to get an account in local bank. From what I understand, it's not just "for the sake of ease", but rather a requirement, because you need to have Finnish account to get salary, pay taxes, get tax refunds, be issued fees and potentially more. I am not sure if you always need it, there could be some exceptions, but it makes sense to have one either way. Since my relocation was handled by Barona, I did not do too much digging into Finnish banks, and just confirmed that recommended OP is fine with me. Maybe that was the wrong choice.

Bank of choice

At the time I did search for information about OP and other banks, of course, and if you check forums, you won't see much negativity. OP is considered one of the best options for foreigners, since their app has been in English for a long time, and they also have multiple service aside from banking, too (investments, different types of insurances, to name a few). It sounds quite reasonable.

Nevertheless, you can find quite a few comments saying, that OP is bad for foreigners because of some racist stuff. The problem is that most (if not all) comments like that are quite generic, lack specifics and overall are not necessarily trustworthy. And you can find similar comments for most of the banks, really. Since you can't really validate those, you need to keep them in mind, but they should not be the main reason you choose one bank over the other. Even if they are true, they can be just anecdotes.

So, I followed my own advice here and agreed to sign a contract with OP. Everything seemed to be working great, I did not have any issues with the service. The only minor gripe was that I was told to come to a branch once I got Finnish ID card, so that it can be stored in their systems and it can fully unlock my account, but when I came in, it was "we don't really need it, because your account is in full mode, no restrictions", but it was still scanned. But this was really minor, could have been a misunderstanding or recent change in procedures, whatever.

But then the war started.

First concerns

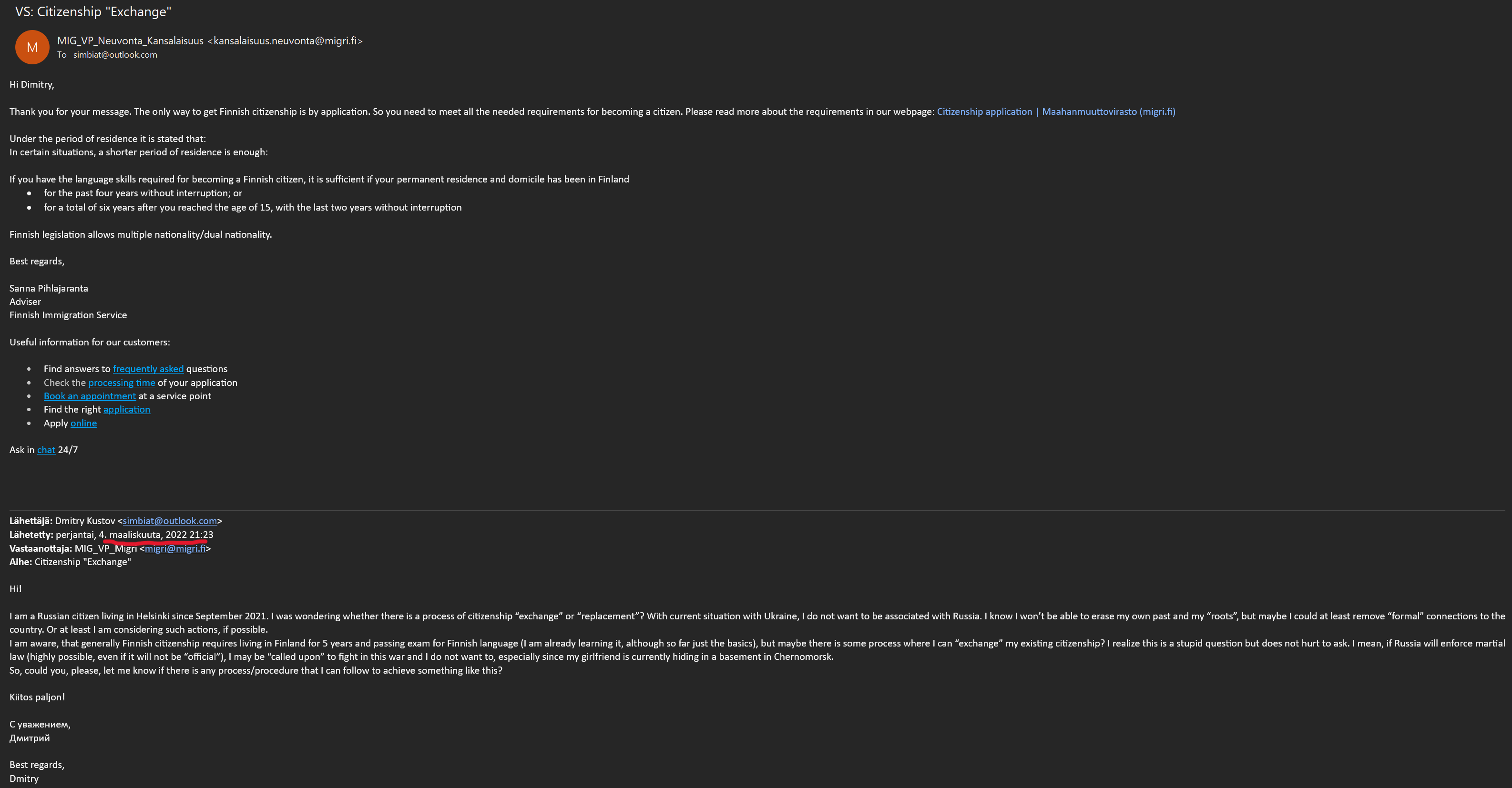

Don't get me wrong, when Russia invaded Ukraine on February 24th, I expected that I will face some difficulties in future because I was born Russian. I expected that in some cases I would need to prove myself. And I did on multiple occasions. Case with JetBrains comes to mind, where my account was temporarily locked, and I needed to provide some evidence, that I do not live in Russia or support the war. I do not remember now what I shared beside my Finnish ID and permit, but I at least shared links to my social media posts about the war, and I think this was also happening after I had game prototype, where you can kill putin, so I shared that one, too. And did the same on multiple other occasions.

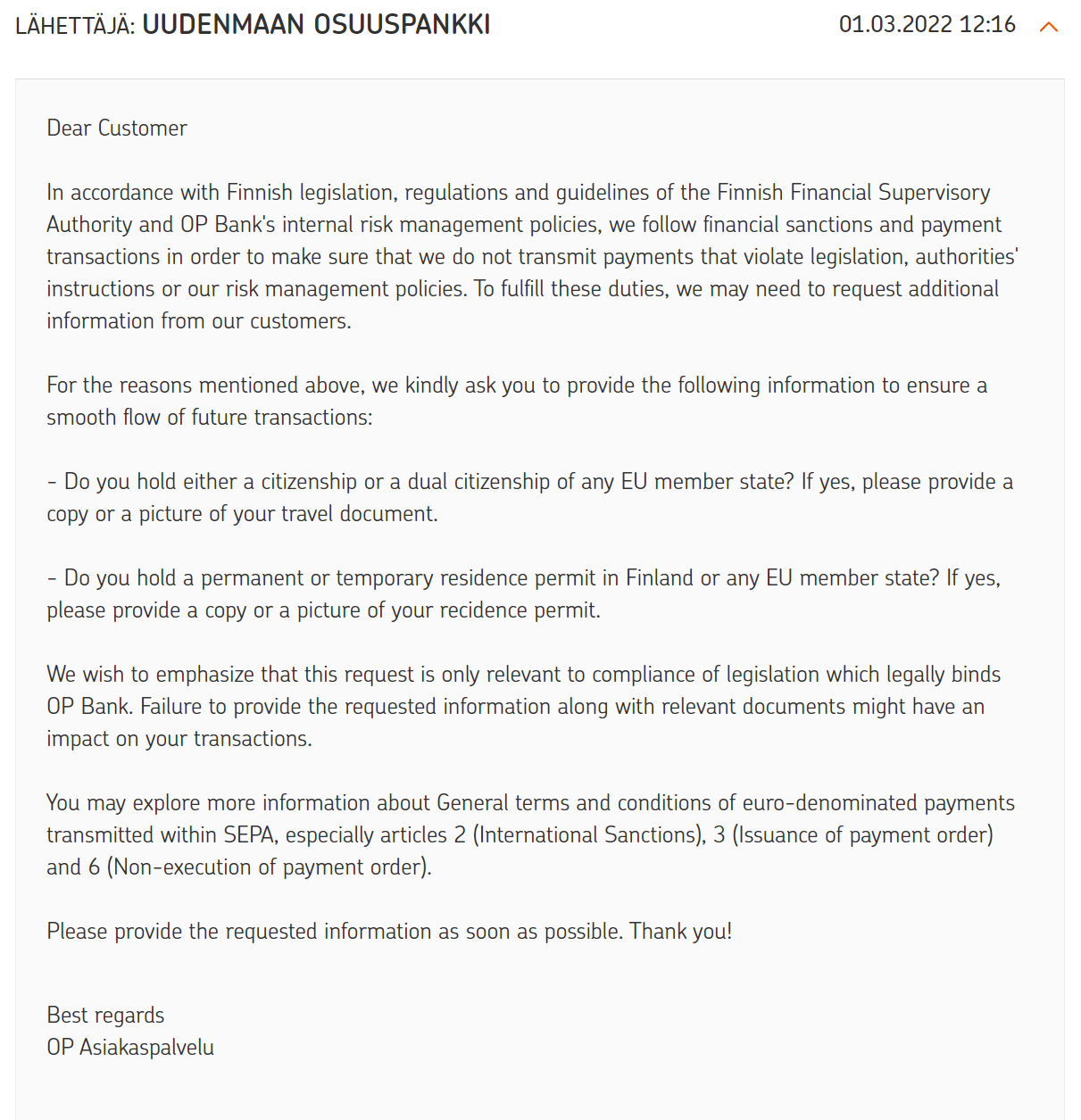

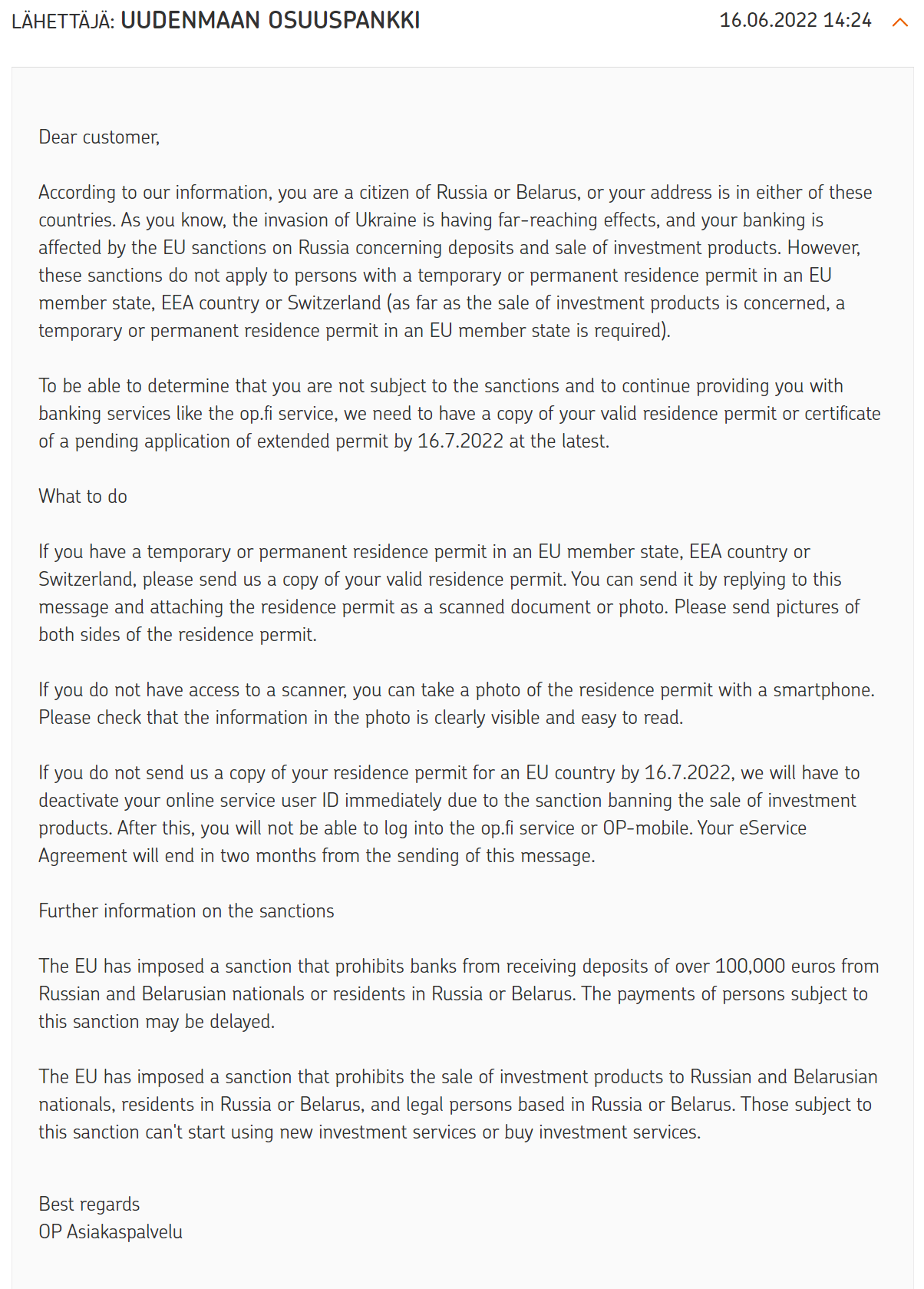

So, I was fine with this. I did not like when my salary was delayed (which was happening for a lot of Russians, as per news). I liked the fact that in OP's chat acted as if they had nothing to do with this, even though officially it was because of sanctions (sadly you can't access past chats, so no screenshots of this one). But all banks, including Nordea and Danske, were playing this game, so hard to say what was really going on and where, and I tried to be understanding of this situation, which my country caused. As such I was not bothered by the bank's request to provide some more information on March 1st, even though, technically, I provided it when opening the account.

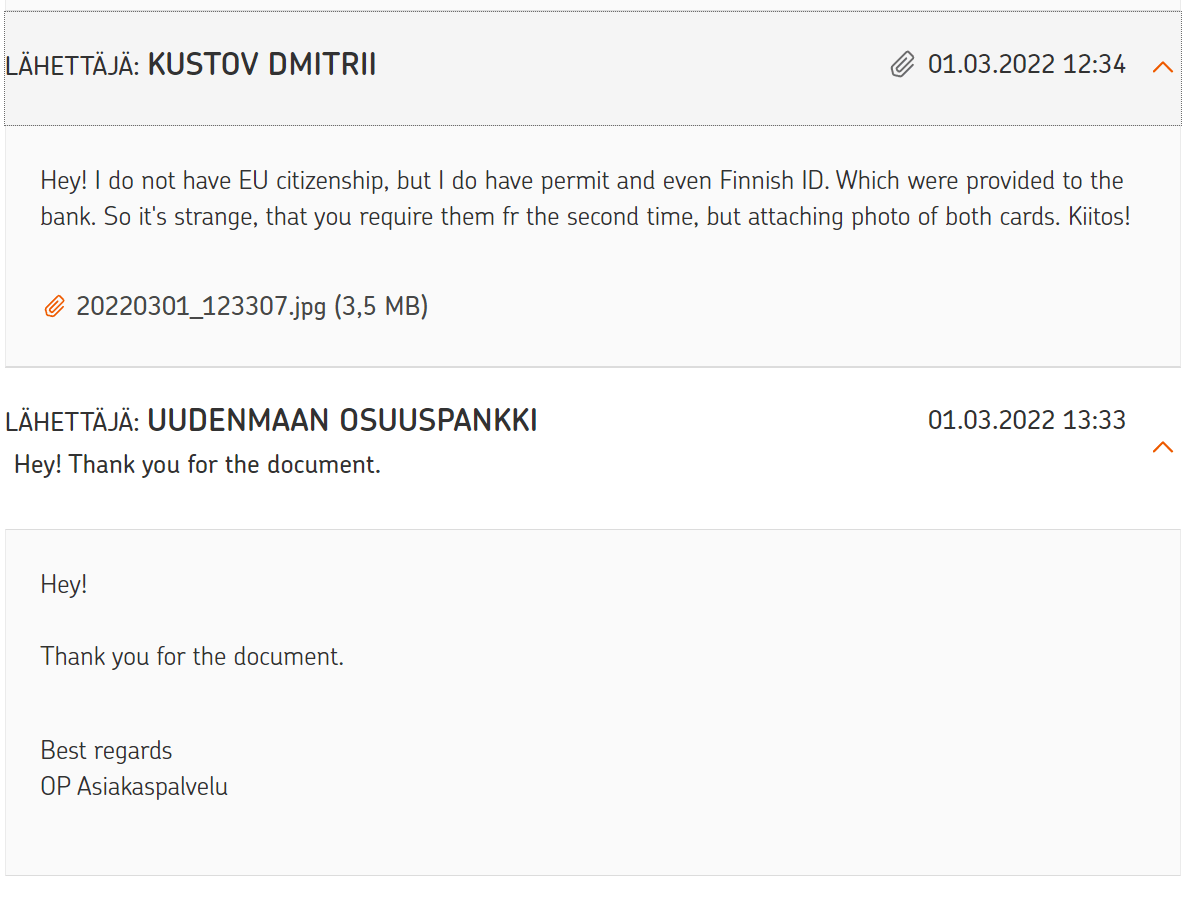

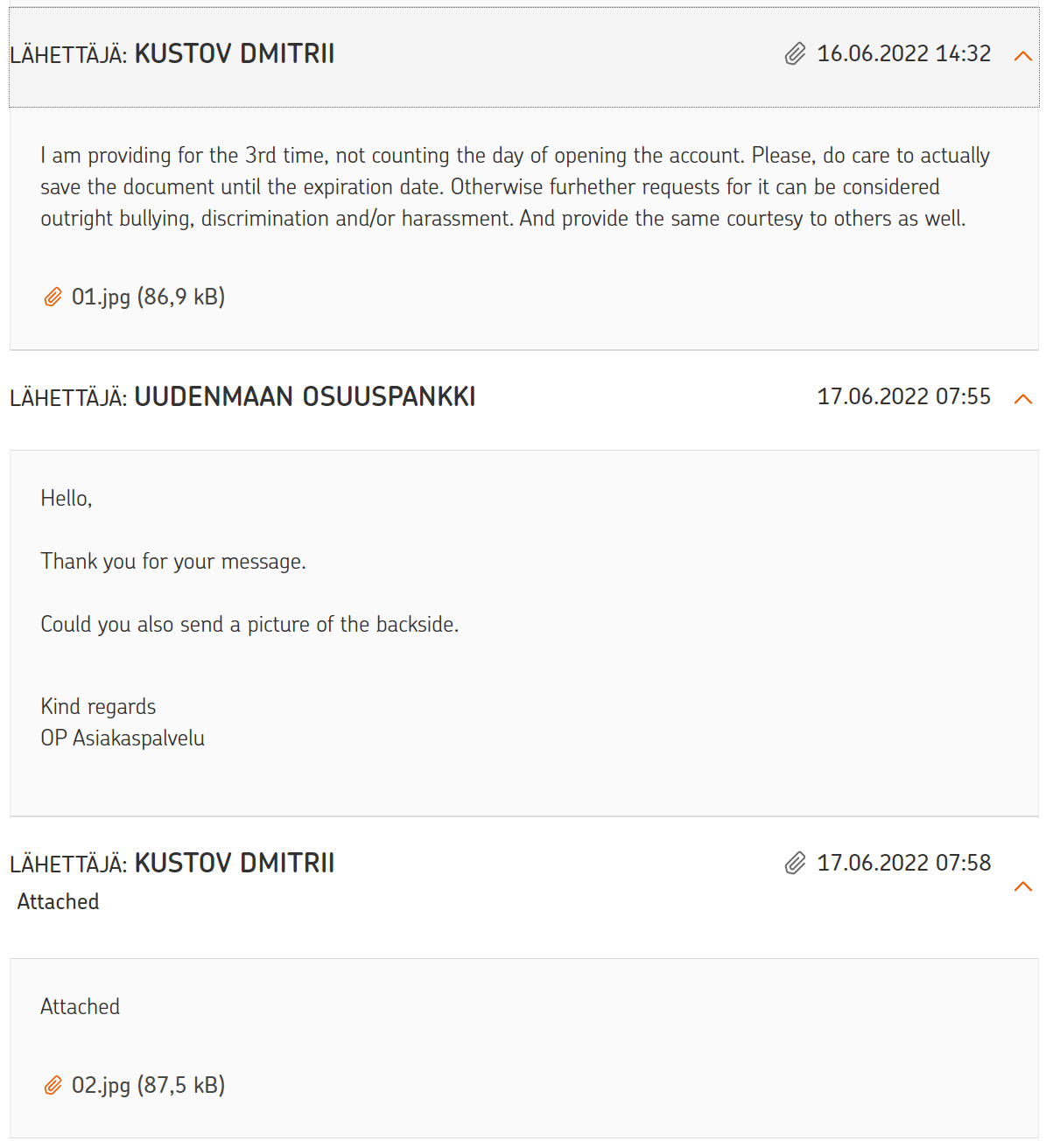

I was mostly fine with the fact that I needed to do it again on June 16th. On screenshot you can see that I complain that this the 3rd time, I believe I shared the details during the chat I've mentioned, too. But, again, since no access to past chats, can't provide evidence of that, but this minor detail does not really matter.

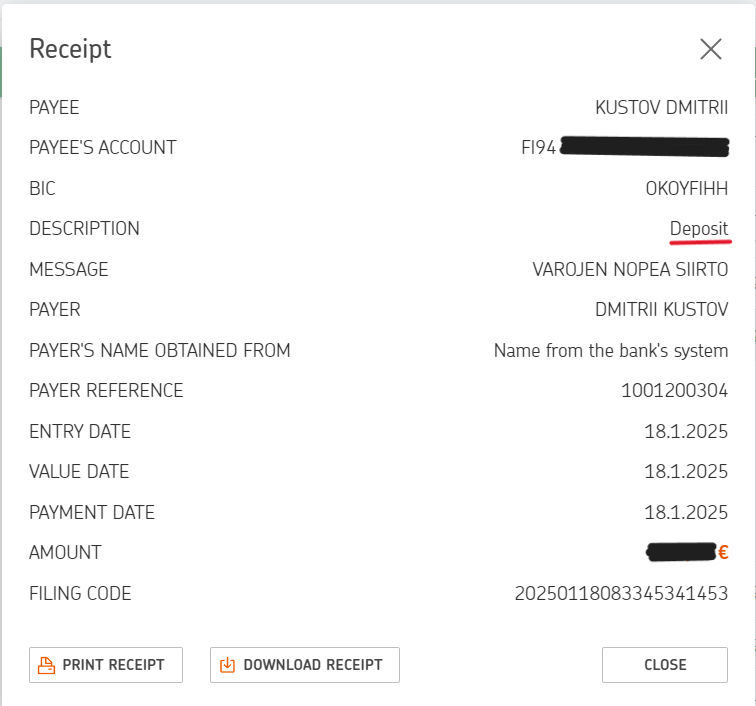

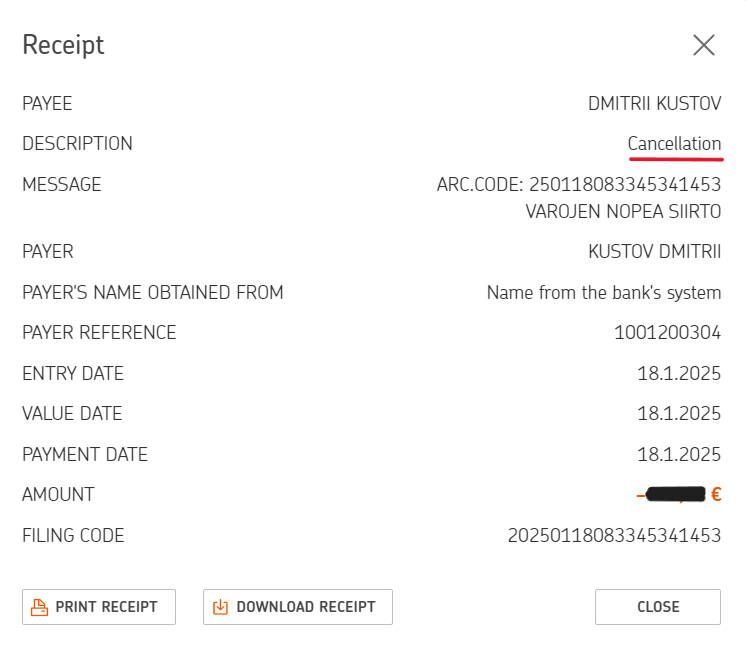

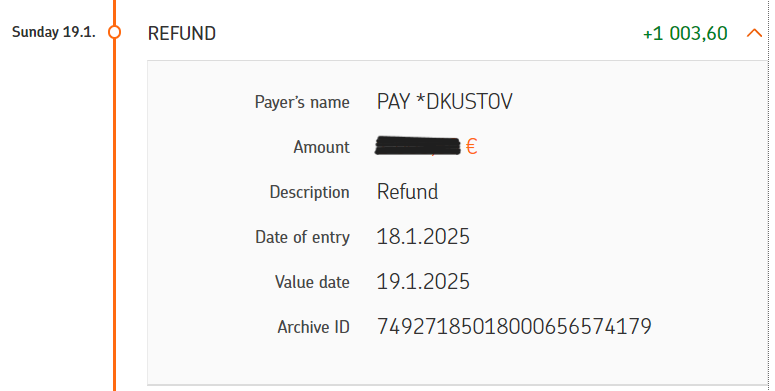

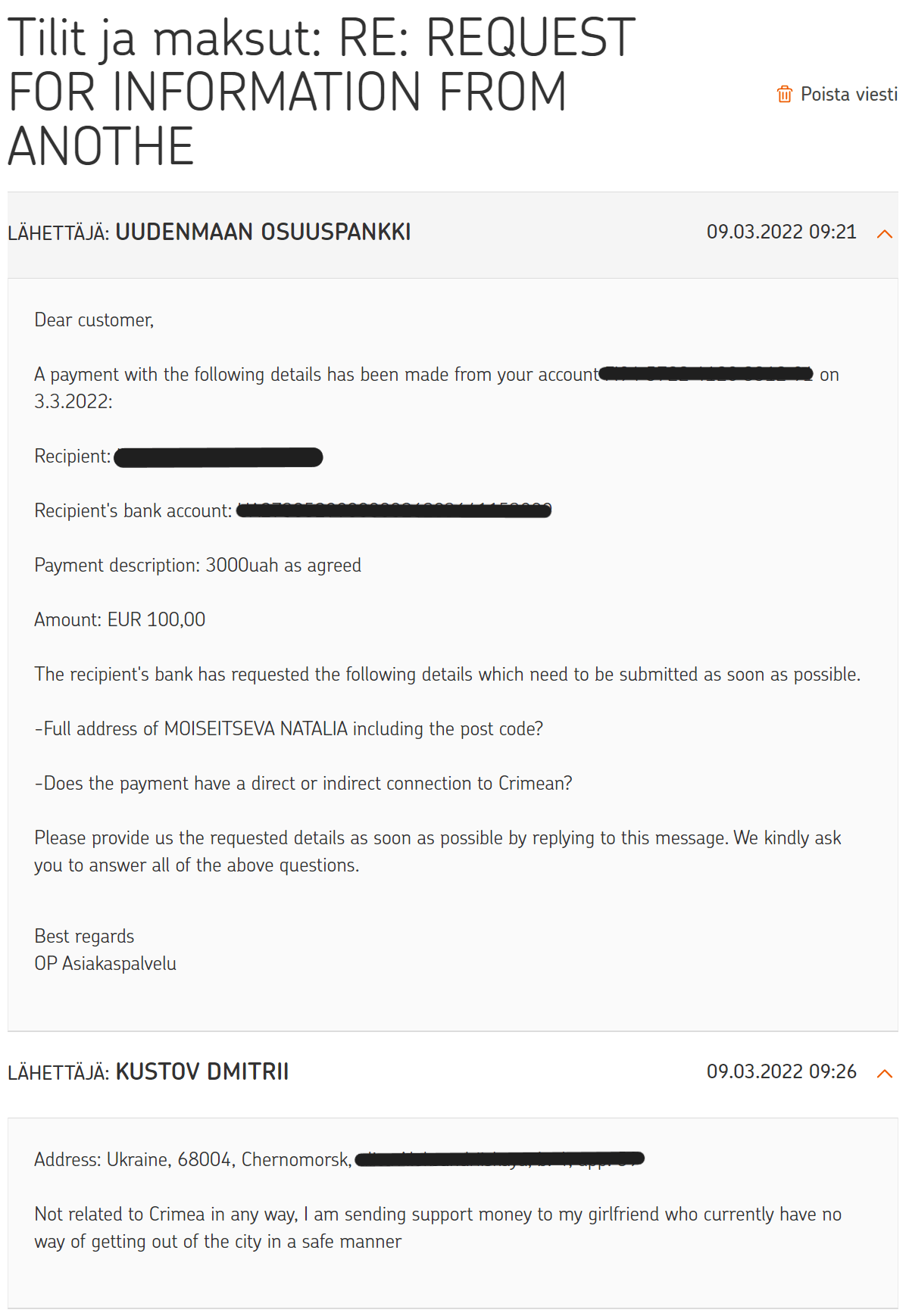

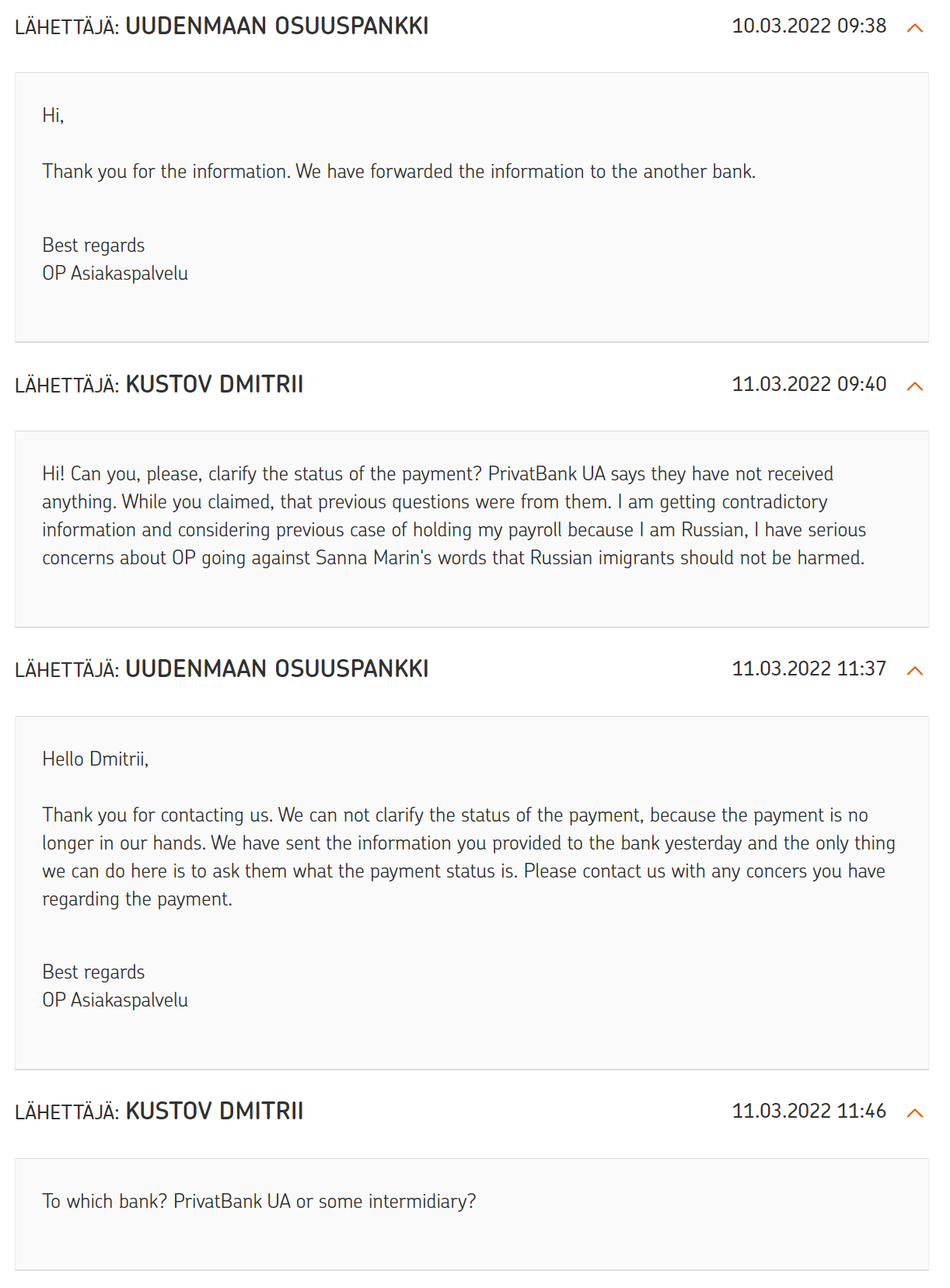

Even when I had issues with sending money to my girlfriend in Ukraine on March 3rd and getting the transaction stuck in limbo, I tried to be understanding. I was annoyed, because of useless responses from OP, as you can see on screenshots, but I could understand it to some degree. Especially, since I do not have a way to confirm it was not a hiccup on PrivatBank's side (they claimed that it's not the case, but they were contacted over phone by my girlfriend, so don't have a recording or anything like that). The money did arrive in the end, I think in the beginning of April or something.

After that everything seemed to be smooth sailing. 2023 went without a hitch, 2024 started out good… Until April. Technically, March, but stuff started happening in April.

Concerns are growing

I have always been a person who tries to save some money. I also usually do not splurge. This is what helped me through my (almost) 1 year of unemployment. This is not something new to me, that happened after I moved to Finland, even though prices here did force me to be just a bit more conscious.

As such I had quite a bit saved on my Russian account in Rosbank. So did my grandma on her Sberbank account. While my grandma was alive, I used Rosbank account heavily, since most things were paid from its card, even when ordering stuff for grandma. It also had more money, so if something expensive was needed it was easier to use it.

But once my grandma died, there was not much reason to keep huge pile of money there, besides paying for utilities in the apartment (which is now rented, and I pay taxes for that in Finland) and for Russian branch of SOS Villages, since they can't receive money from abroad right now. And thus, I did the most logical thing: looked into ways to transfer money from Russia to Finland. There are not that many ways to do that, and honestly, I simply do not trust crypto and the semi-legal (and sometimes fully (i)legal) stuff around it, and luckily around this time one of the people from Smartly.io, whom I will not name, unless the person will want to come public, needed to get a lot of rubles…

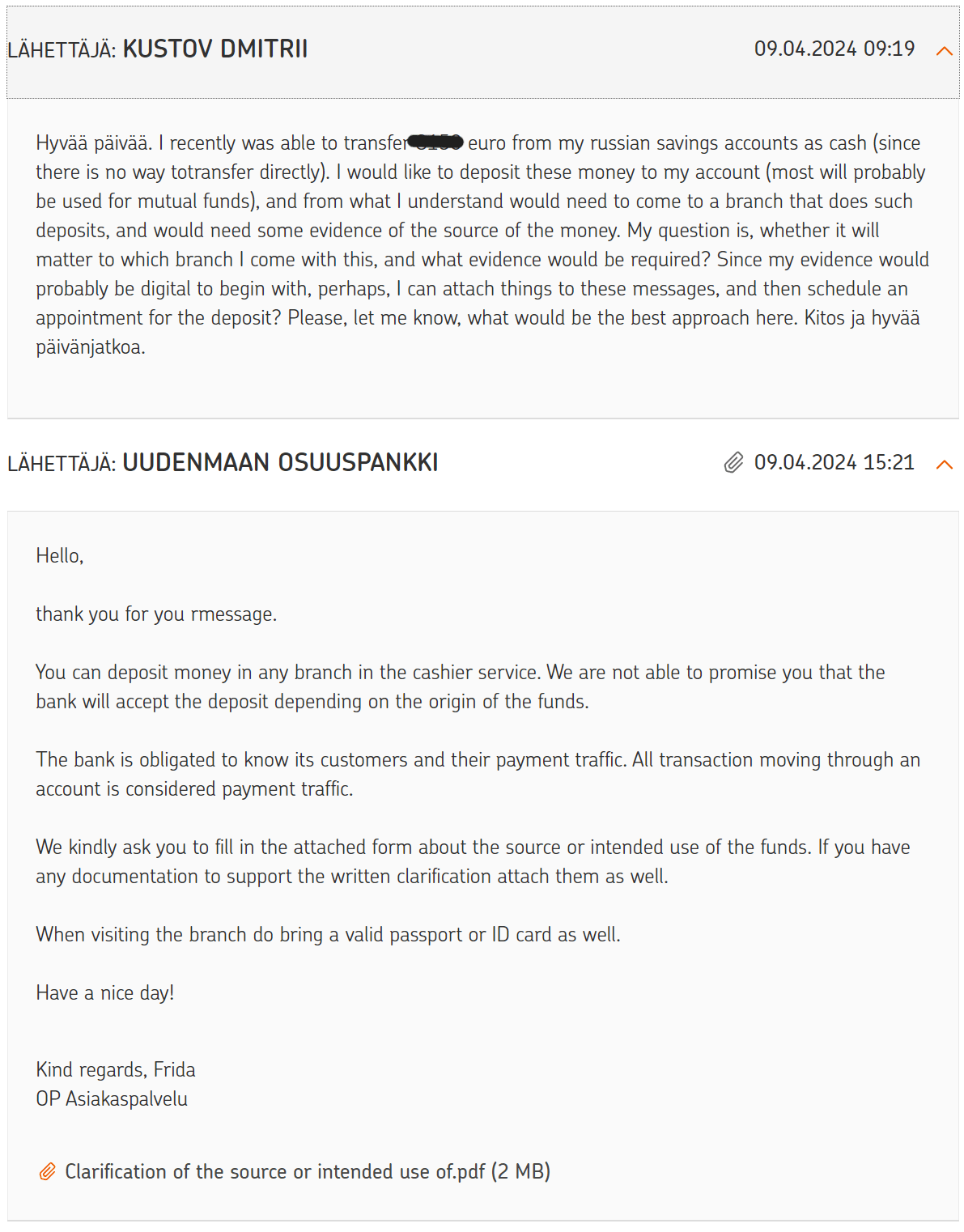

Since the person was actually converting money from USD using an ATM (I think in Georgia, but not sure), we had to use cash. Essentially the only other legitimate way to convert rubles to euros at the moment. Of course, it is also problematic. For starters, I did not want this thick cake of cash on me, I would prefer it "working" on some mutual fund or whatever, to get at least some profit, while it's lying there. But you can't deposit more than 1000 euros at once, unless you submit some form to the bank and come to the branch. Knowing that, I reached out to the bank beforehand. Multiple times but only in April I got some response.

I filled in a form, there is nothing much there, the only relevant thing would be explanation of the source: "From personal saving account in Rosbank. Conversion done through a friend: I sent rubles to him; he withdrew euros from his account. Money was accumulated over the years, with a percentage transferred recently from account of my late grandmother. Purpose is to partially use as cash buffer and partially invest (most likely mutual funds)." I also shared an account statement for my savings account dating back to April 2019 (could not get older through Rosbank's app).

This is not visible on screenshots, but I got a call from OP on, I believe, April 10th. It was verified through their app, so it was legitimate. I was told that everything is, essentially, fine and we agreed on a date when I come by to the branch to deposit the money. And I did come on the date, as agreed. Waited for like 2 hours, before I got into a booth, because for some reason most of operators were away (felt like I was back in Russian Sberbank or something).

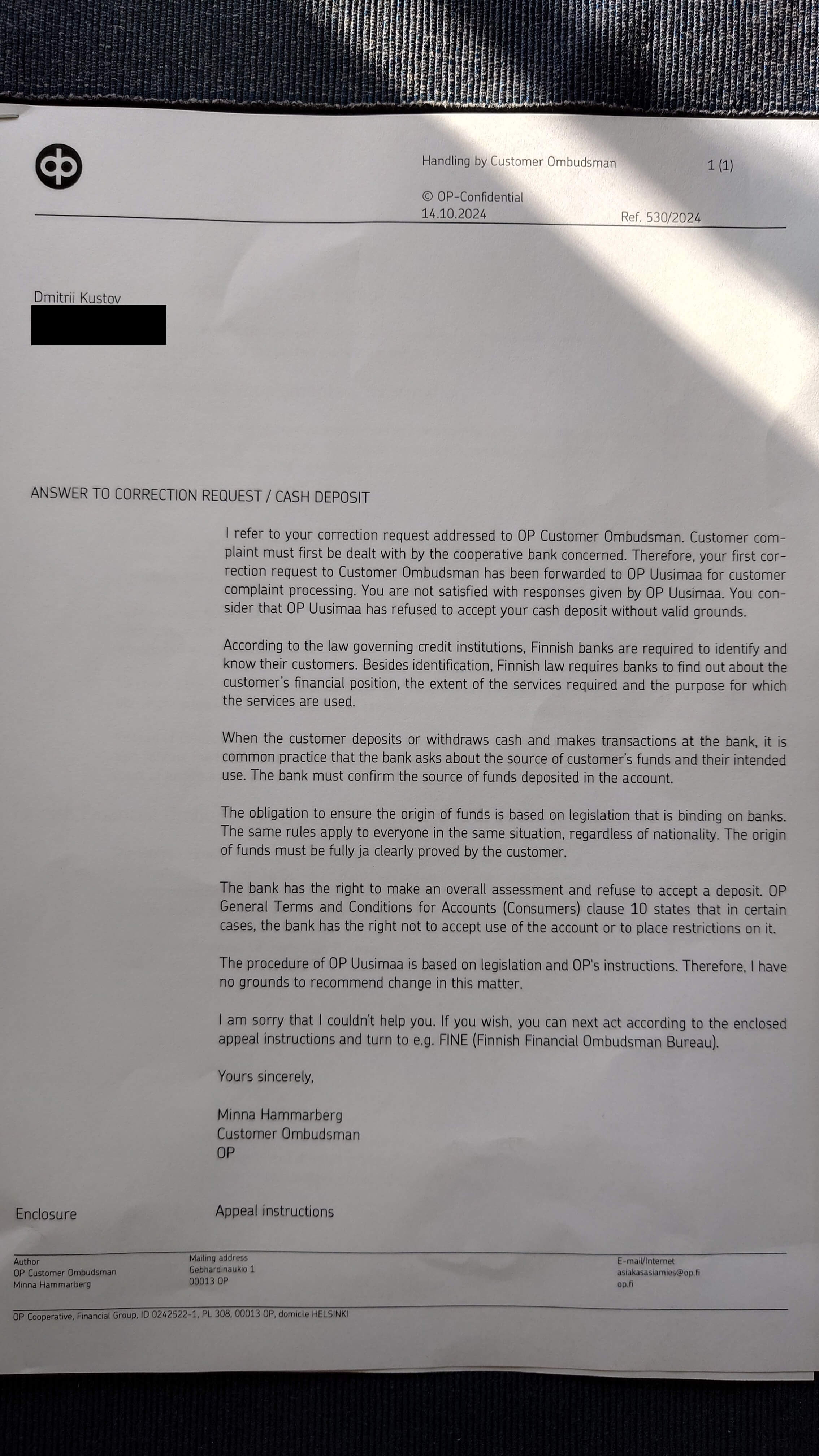

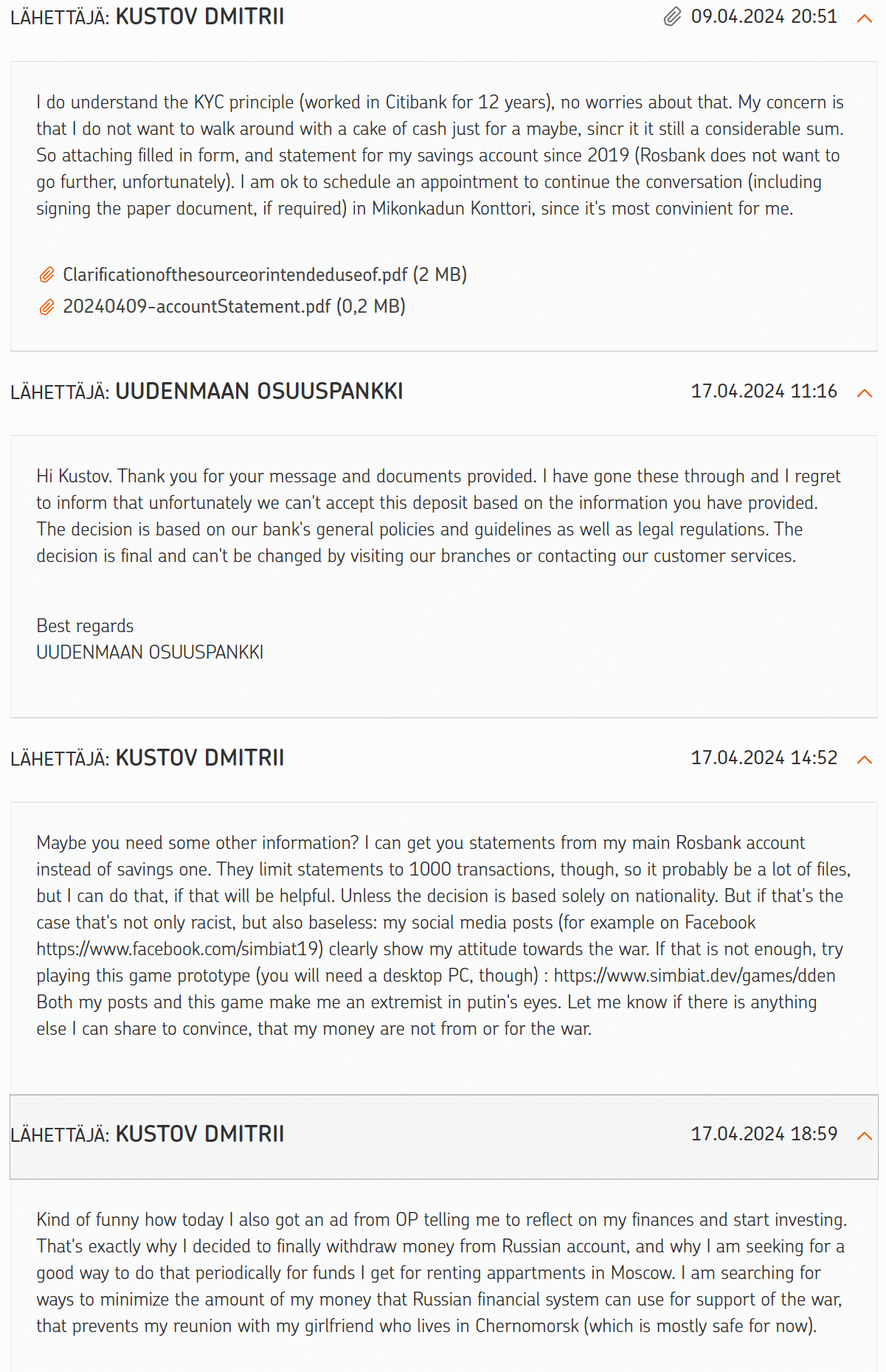

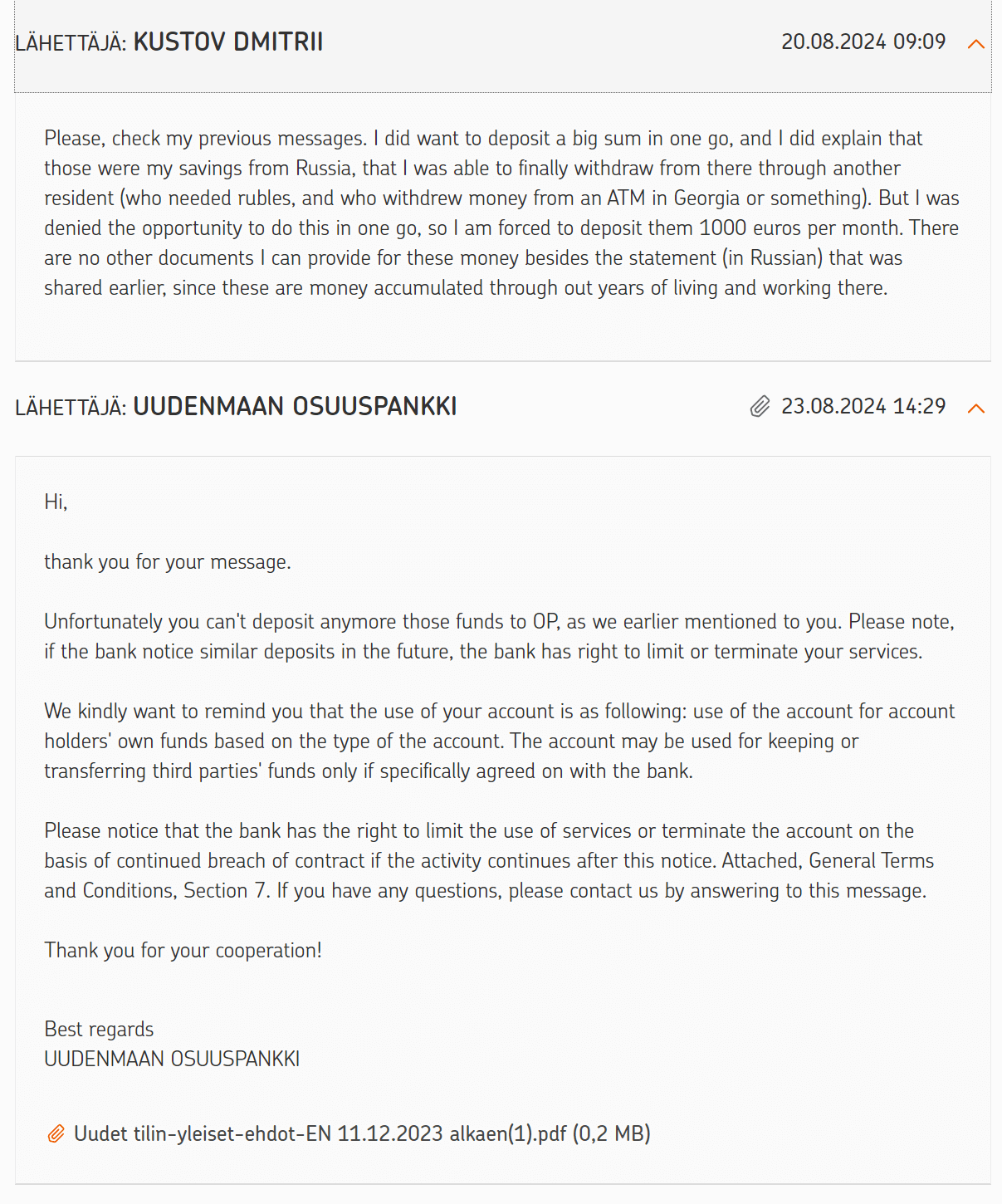

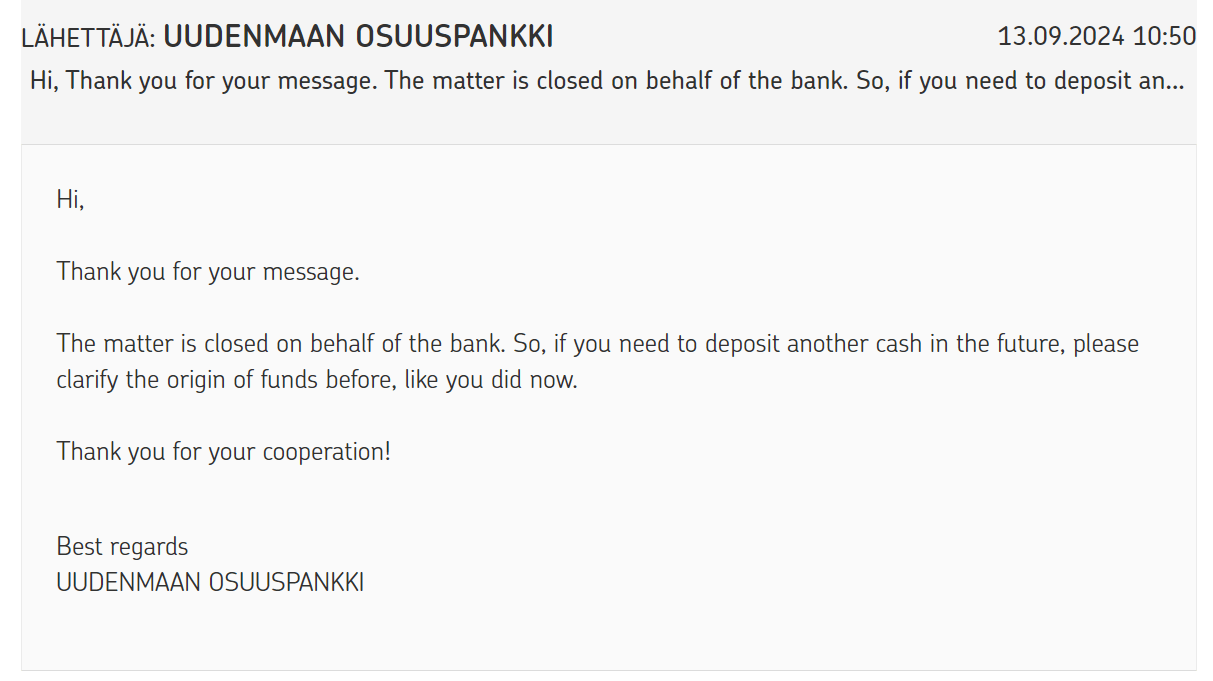

There I was told that the girl that called me was mistaken, and they still needed to validate something, and then I would receive a message, and only after that I should come. As you can see on screenshots above, I did get a message, but it quite firmly said "no, matter is closed", and was ignored, when trying to establish contact again. So, I thought: "Ok, I will then deposit 1000 per month, even though it's a pain in the butt", and moved on with my life.

The meat of the matter

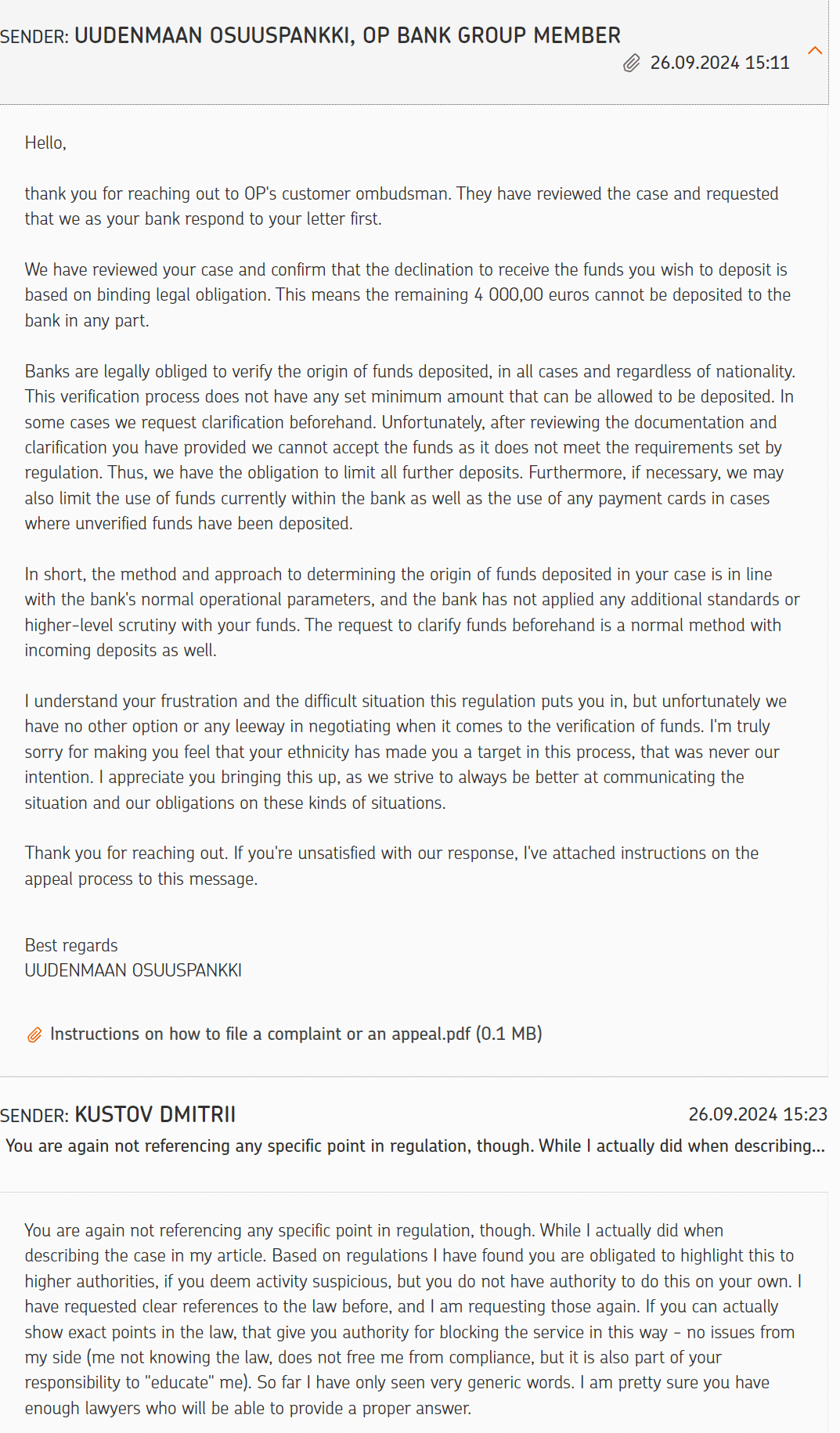

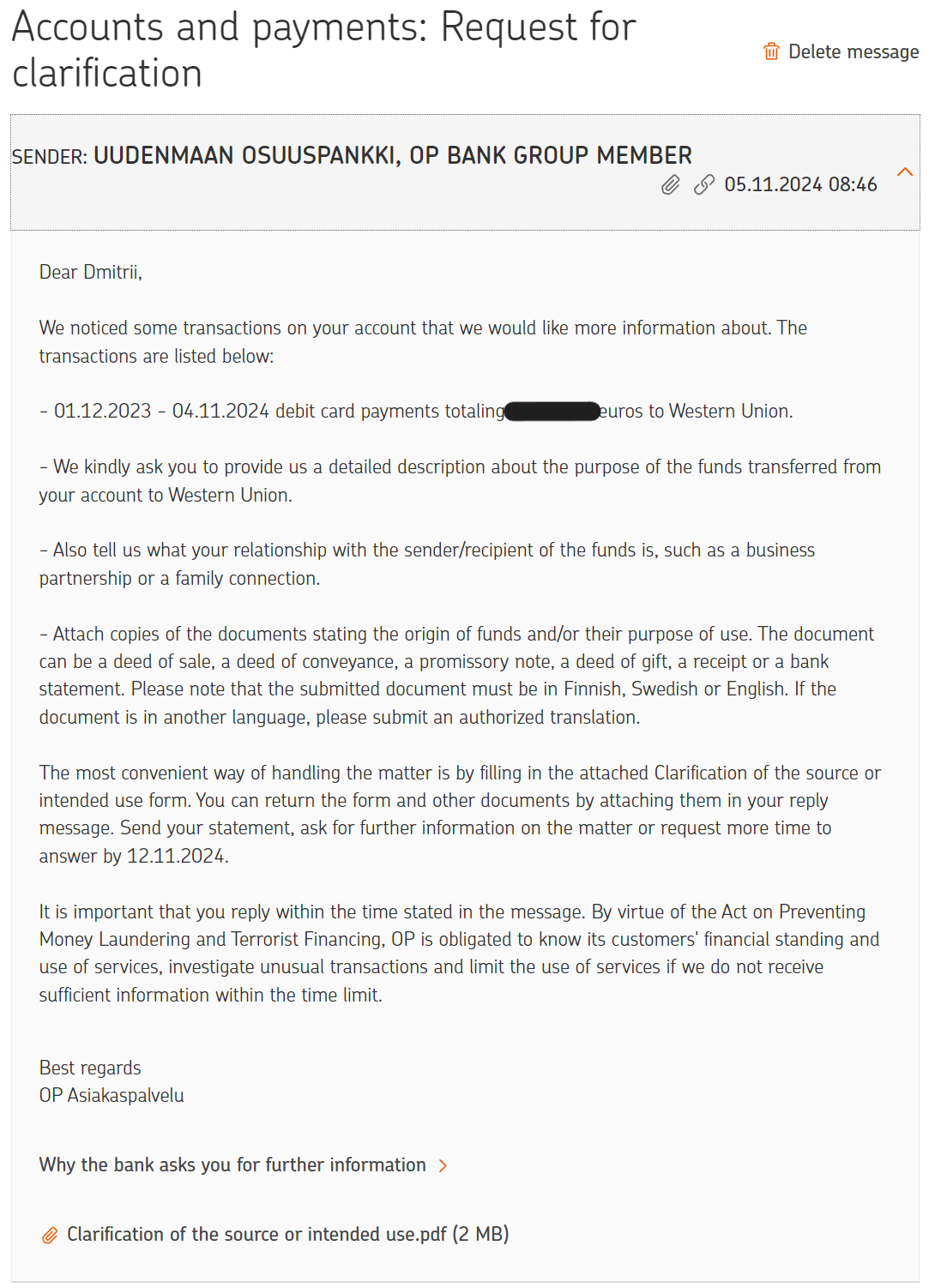

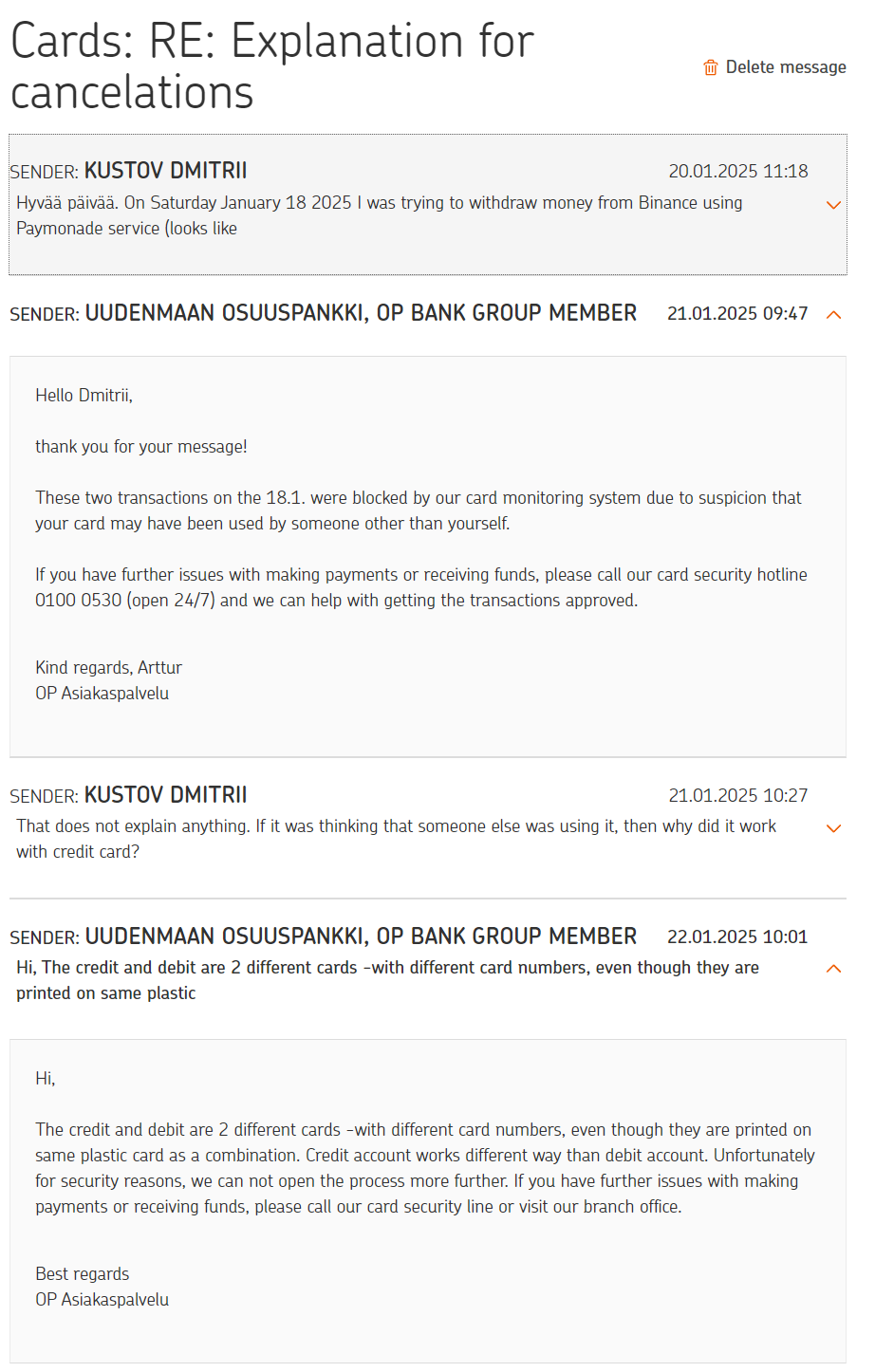

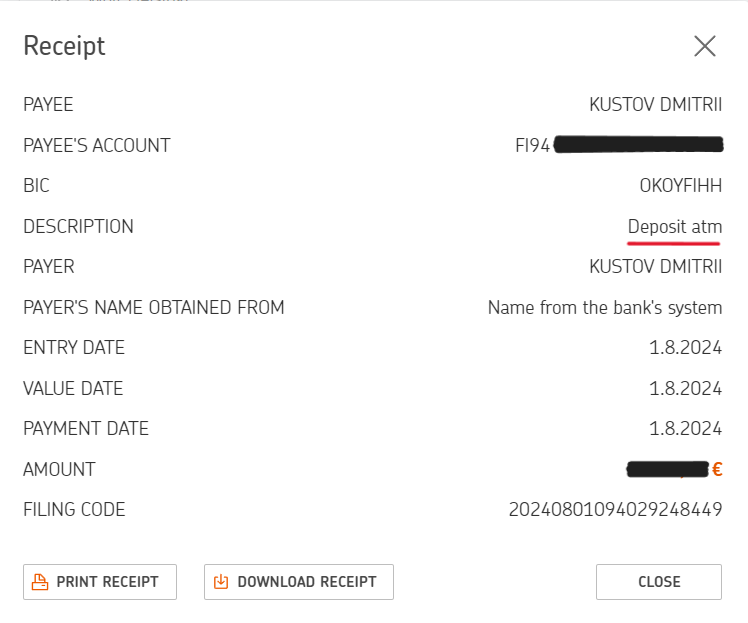

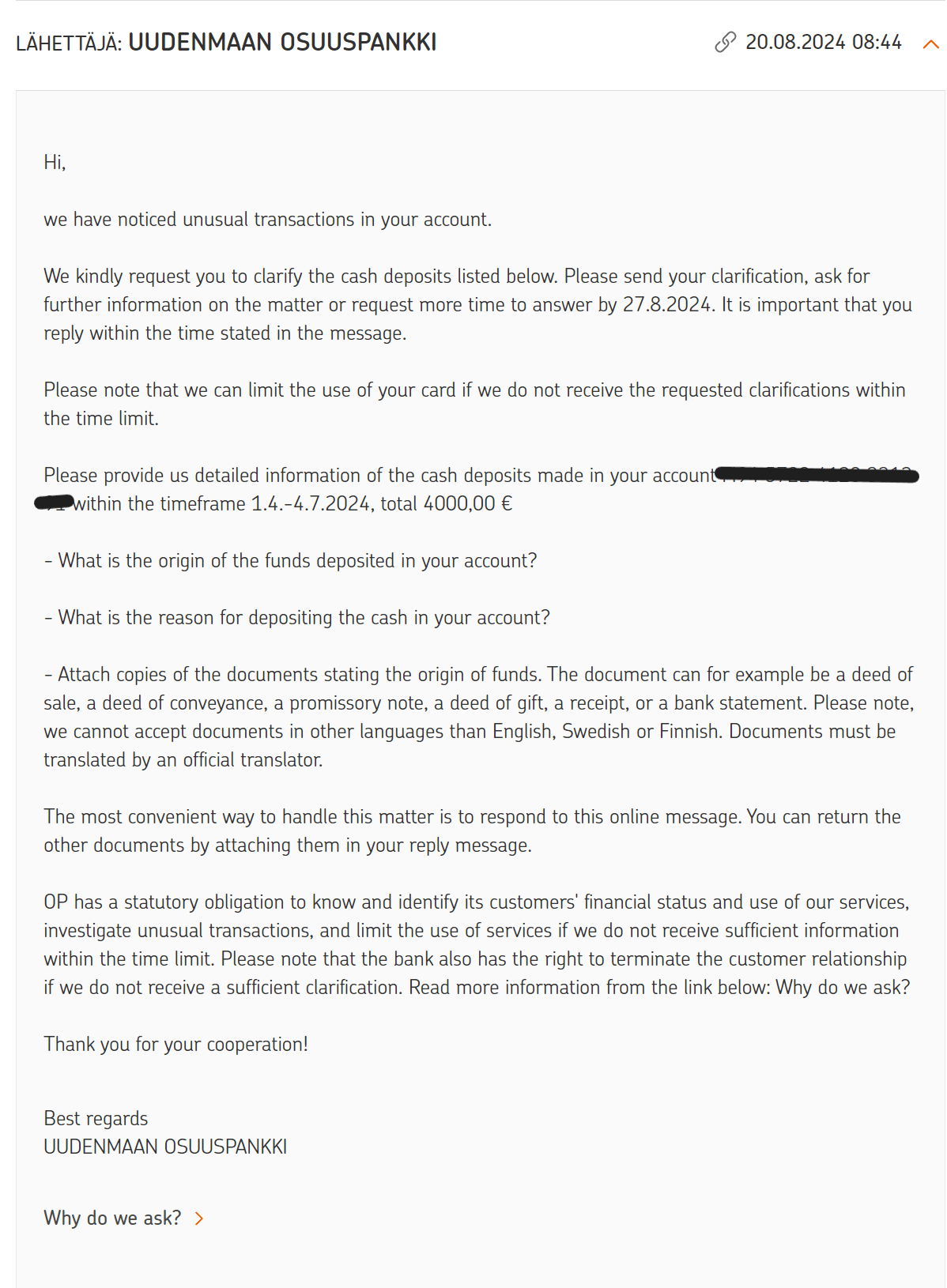

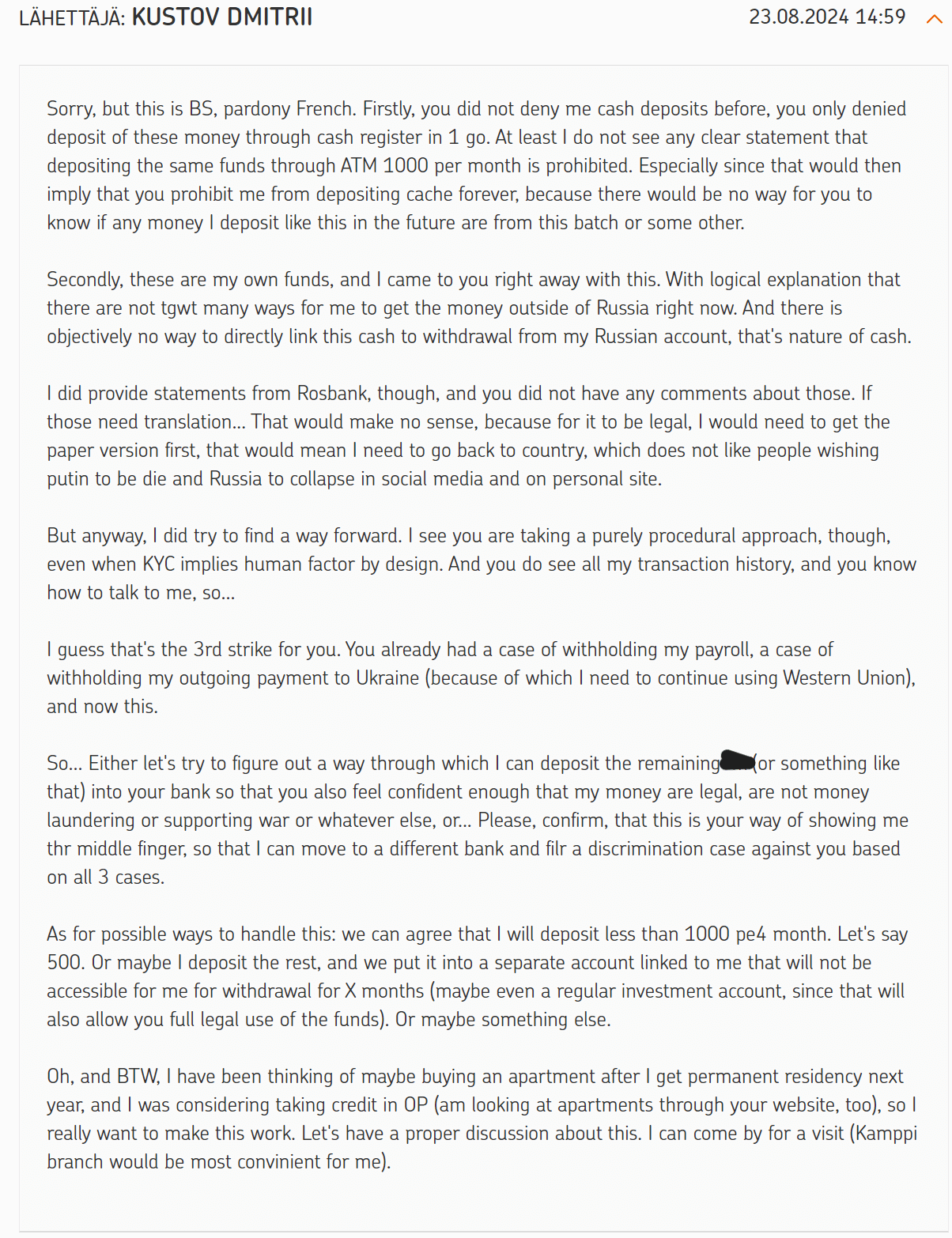

But all of this is essentially a prelude, even though it has some context, importance of which I will explain later. The main issue, because of which I decided to write all this in the first place is: on August 20th I got a message from OP asking to… Share details about cash deposits from may to July (for some reason they did not include August).

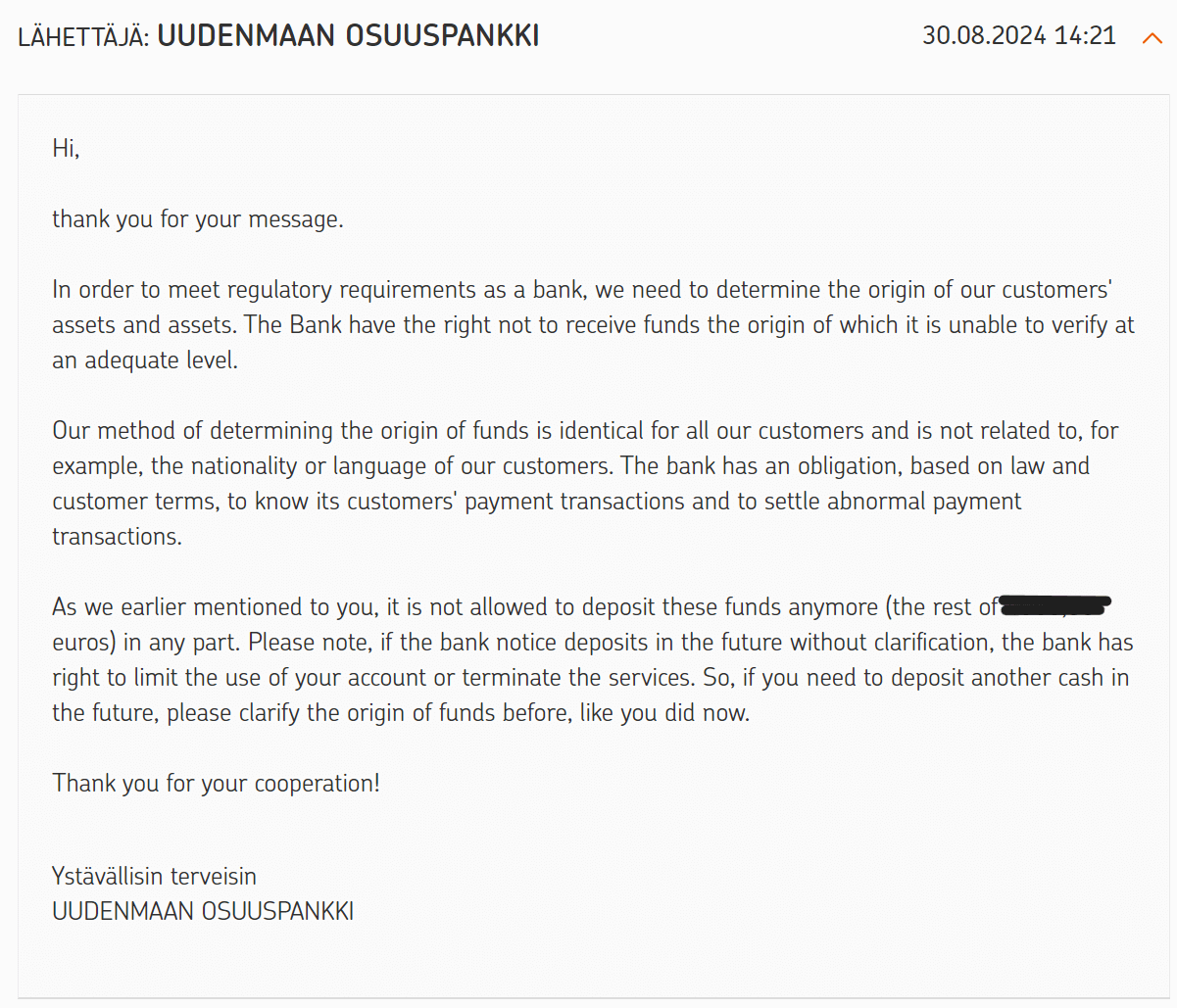

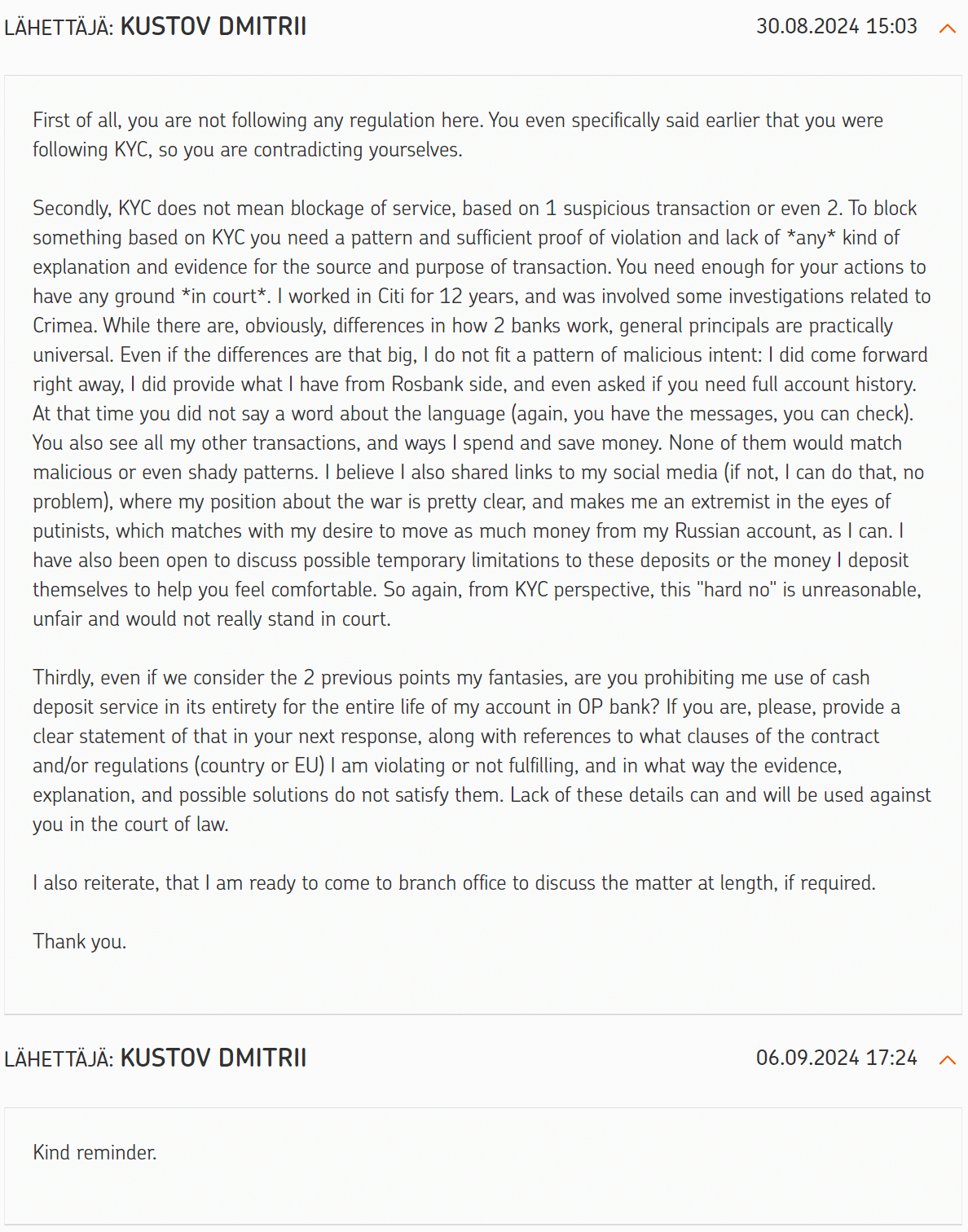

Essentially, they were asking for the same thing but with a new requirement of evidence being in English (which is important point, I will get back to it). You can read the whole conversation on screenshots, but the gist of it is, that "because of KYC" ("know your client") they denied me any further cash deposits under threat of terminating my account entirely. Trying to find a reasonable compromise failed.

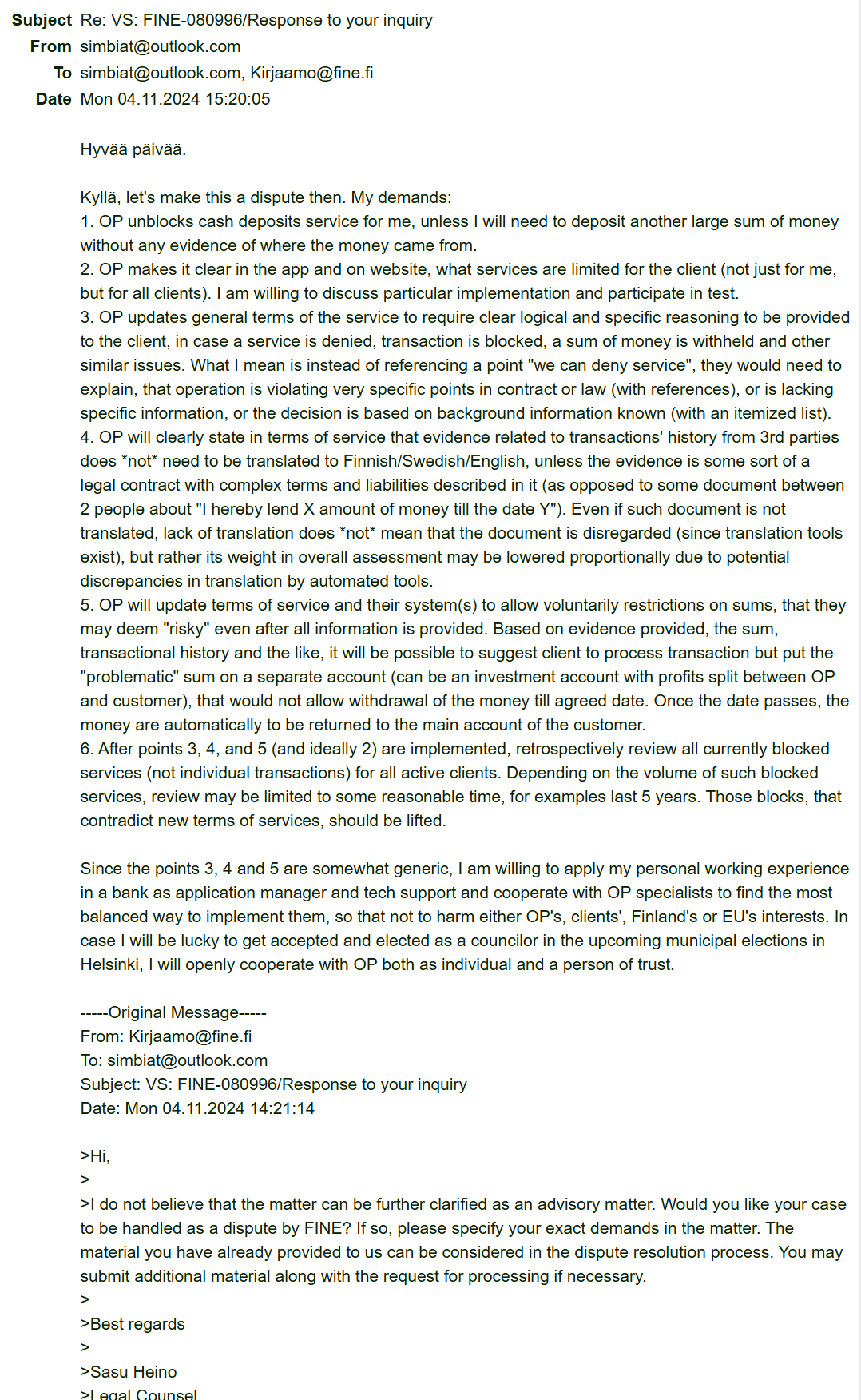

Were my responses "highly professional"? Probably not. I was frustrated. Was I justified in my frustration? I think yes. Will I just swallow it, as some people expect all Russians to do (while looking at what is happening in Russia)? No. I am not a lawyer or anything like that, but I do know how to read, and I do believe, that this matter is… Not good, let's put it this way for now, and I will go through everything soon. Before that, I would like to point out one important thing for some people. Those people will probably not even reach this point in the text, but still.

I am not asking for special treatment. I am not asking for a privilege. Having a bank account with all related services is not just a right in the modern world, but a necessity. Threating with its closure with weak justification is something that Russian "politics" and "bratki" would do. I was (and still am) ready to negotiate some temporary limitations, and this is a very important point.

What I am asking is equal treatment based on actual data the bank has on me, and not based on my nationality, which I can't easily change, even if I want to.

Know your client

If you agree with me saying this is a bad situation, and the bank is in the wrong, you may wonder: "Is this legal?" I would say it's kind of in a gray area, which I will explain later. What I can tell right away is that OP's claim that they are doing this as part of KYC is wrong, because KYC does not allow them to block anything. At least not by itself.

For those who do not know KYC is part of AML (anti money laundering) framework, which includes various processes and legislations to prevent, track, block transactions that benefit "bad actors", and punish those bad actors, when possible. The whole framework can seem quite complex at a glance, but at its core is KYC, which is a set of best practices, often times described in local laws to some extent.

The basic idea is that you need to know the person or business you are dealing with. At the basic level this means identification, authentication (and resulting authorization, to an extent, at least). That's why when you open a bank account or card you usually need to provide a passport, a driver's license or some other sort of ID. It may also require extra information like main sources of income, where you come from, where you live, whether you are married, have children, etc.

At the same time, it's not a one-time thing. Besides regular authentication through password or biometrics or one-time codes (which are obvious), KYC includes monitoring of transactions for potentially suspicious activity. Or to be a bit more correct: for suspicious patterns. It may not be just 1 transaction, although if you write in description that you are buying AK-47 it will be flagged. In some cases, you will need a set or series of transactions that look abnormal compared to your previous regular transactions. Like in my case – regular cash deposits of 1000 euros, since I did not do those before (did not have a need).

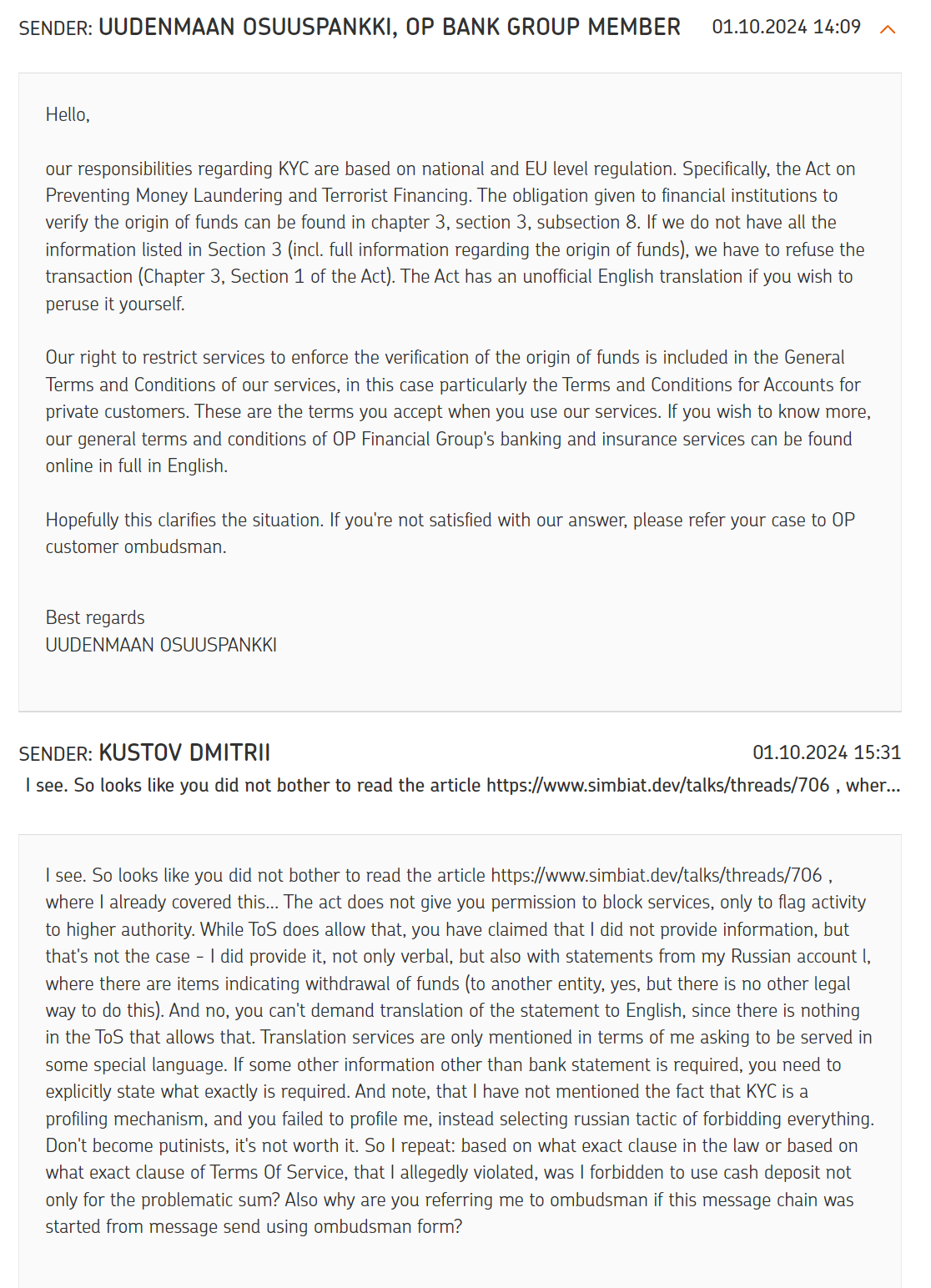

In Finland main law about AML, Laki rahanpesun ja terrorismin rahoittamisen estämisestä, covers various rules for KYC as well. If you do not know Finnish, Google Translate seem to do a good job translating the page to English, since it's in formal language, so it's relatively precise. Law even mentions requirements for more rigorous KYC processes, which include "high-risk countries". I was not able to figure out where to find a list of those countries, but Russia is probably in it now.

So looks reasonable to ask questions of me, right? And it is. This is something I totally agreed with in my messages with the bank. If a pattern is found, you need to get more context and require as much information (verbal, written or otherwise) to have that context, and make assessment. Here's the catch though: the law does not give a bank (or any other entity) the right to limit account activity, let alone terminate accounts at their own discretion. They are obliged to report this activity to supervisory authority, that is FIN-FSA, as per chapter 3, sections 4 and 5, at minimum, as well as Laki Finanssivalvonnasta. Unless I am missing or misinterpreting something. But I did work in a bank, too, and Citi seemed to have some requirements across branches.

Legally grey

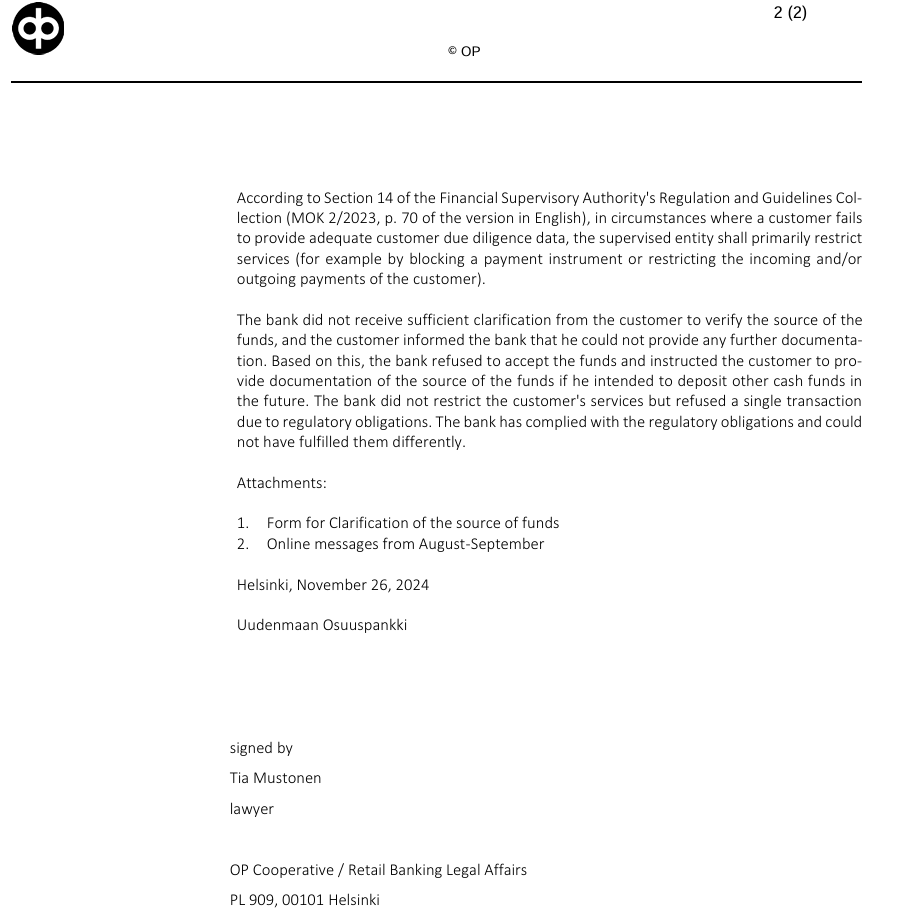

So where is this coming from, if KYC is meant to be profiling and reporting framework? In the message they referenced (and attached) "General Terms and Conditions, Section 7", but it does not have anything like that:

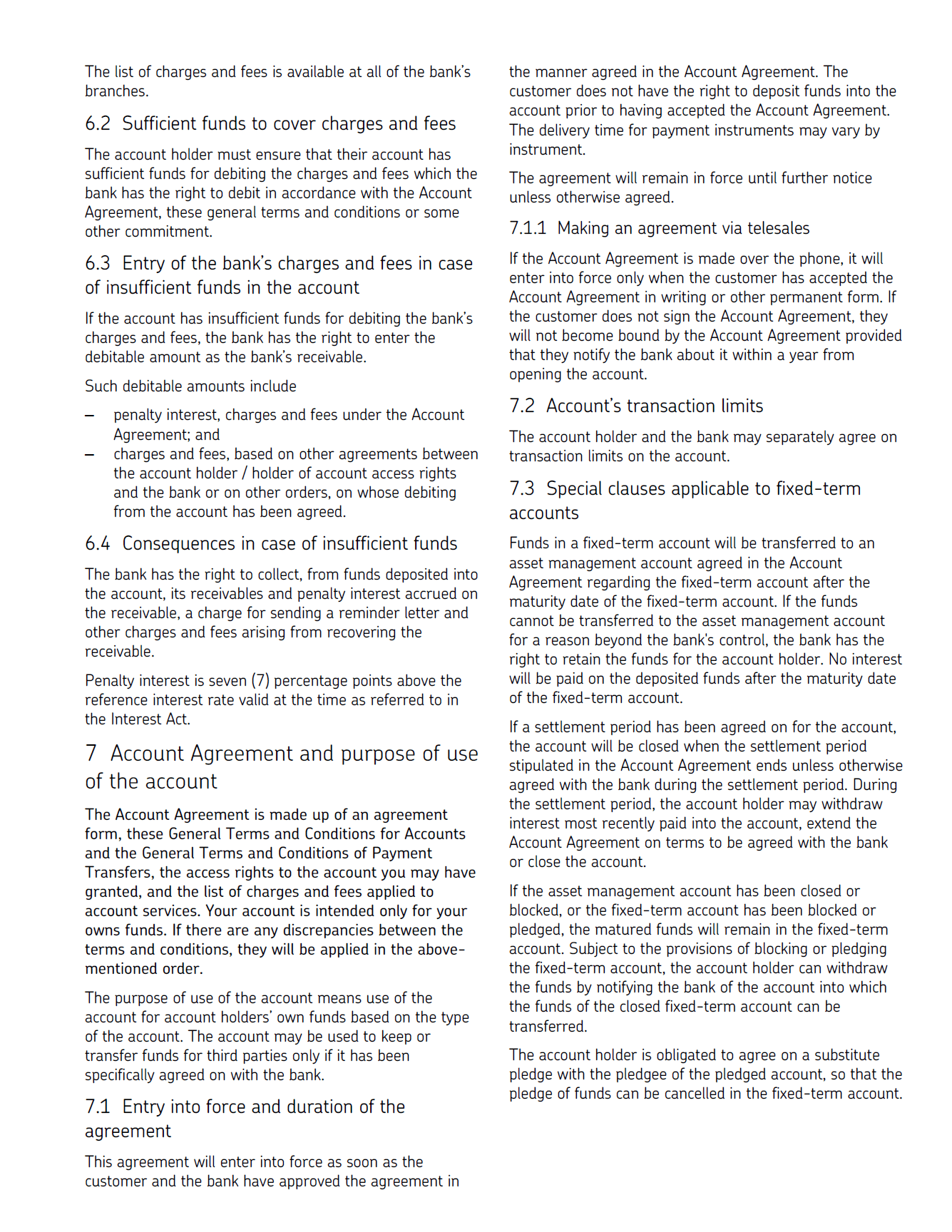

It is kind of related to KYC, but I do not see anything about restrictions or termination. They also referenced this Why We Ask link, which is pure KYC, and it even has link to FIN-FSA's page about the same thing, which still does not give permission to block transactions or terminate accounts, for existing customers – only inquire. So, what is it then? Well, there is something in "General Terms and Conditions", specifically in version that came into force in April 2024 (for existing accounts), specifically Section 10:

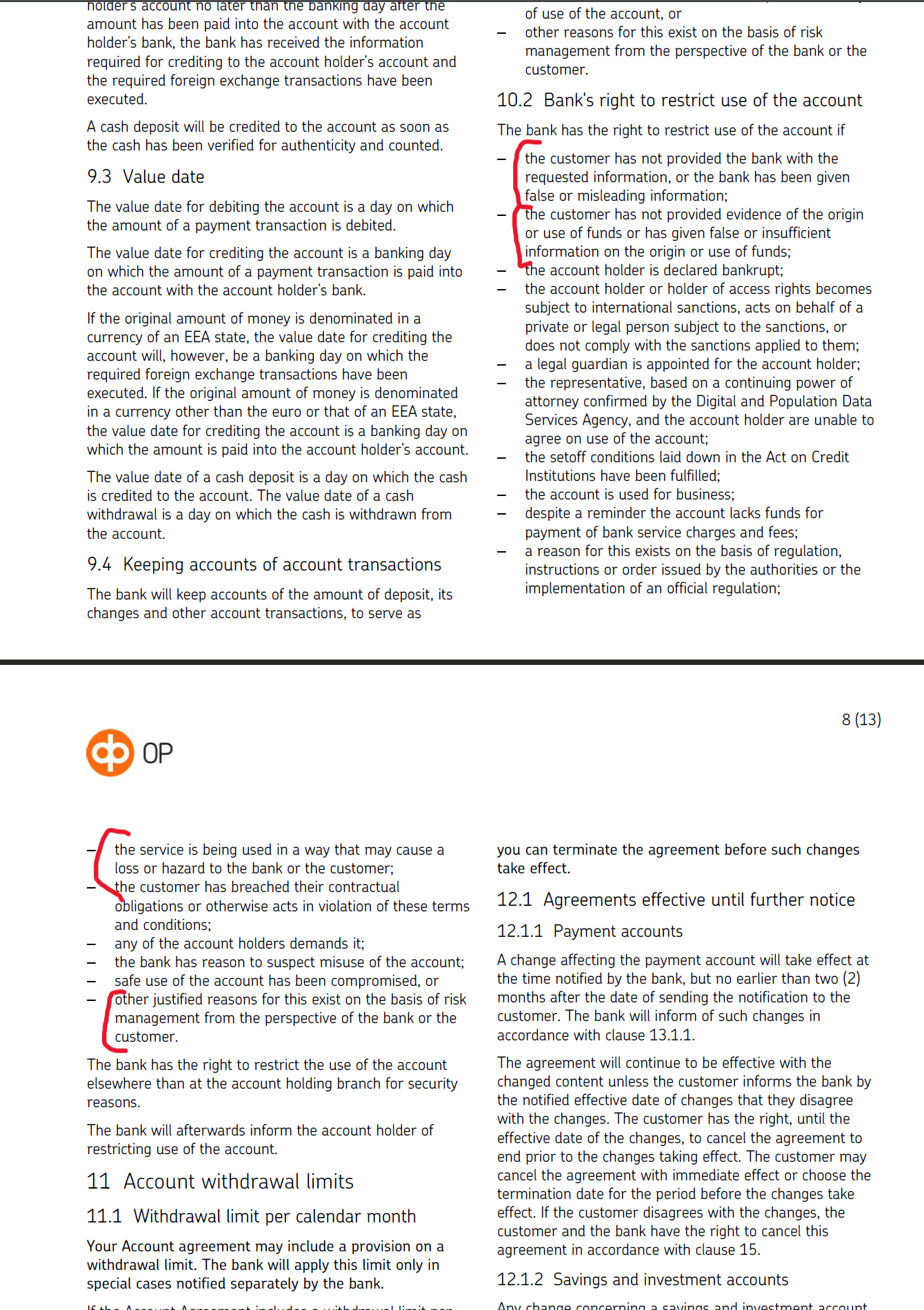

For reference, same section from when I signed the contract in September 2021 (there does not seem to be any changes in between):

Notice how many items were added to the new version and how relatively vague they are. Originally only "the bank has reason to suspect misuse of the account" was vague (which was already enough to be misused), but now there is even more. For my case the first 2 items seem to be most relevant, and they can be read as "we can request you to provide information on Egyptian parchment written in virgin unicorn's tears, and if you do not – bye, bye, bye".

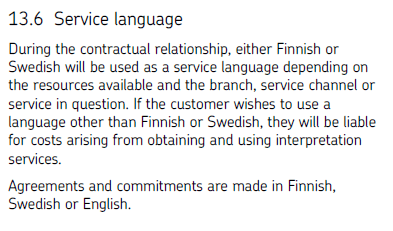

I am exaggerating, of course, but where is the definition of "insufficient information"? If it's not clearly defined, you can make up anything you want. And if that's not enough for you: do you remember me mentioning importance of OP requesting information in English when they approached me in August? Not only does contradict their own Section 13 (on screenshot below), which at least does not prohibit use of other languages and does not require evidence to be in specific language, but even violates linguistic rights, which are explained on this page from Finnish Ministry of Justice and are part of constitution.

Racist much?

One may say something like: "Don't you know banks? They will do whatever they want to screw people over!" That is true to an extent, but they do need money to operate, so rejecting more money in accounts owned by the bank sounds a bit illogical. So why do that? I can only see 2 reasons, that would make some sense to me: either overcompliance or racism. Or a mix of both.

For those who do not know, overcompliance is when an entity does something not required by law, but what it thinks will cover its behind. You probably saw those cookie pop-ups, asking to confirm, that you agree to use them: it was claimed, that this is required by GDPR, but that was never the case, it's just most decided to implement this annoying feature "just in case someone will complain" (and because it was simpler than not storing user data in cookies). Since I am objectively in a "risk group" because of my nationality, and there are sanctions, and we know how Russian entities like to abuse things and cover up things and whatnot, it does make sense to be a bit more cautious even with seemingly regular people.

But as I said, there was a reason for a long "prelude" in this story. I would call it "KYB" (know your bank) or even "KYSP" (know your service provider). I collected this information specifically to profile the bank, same way they are supposed to be profiling me. Having a set of incidents, which are related to my nationality specifically… I hope you can see how this can look like racism. Knowing, that I am far from the only one (and not talking about Russian, but foreigners in general) – only supports the case further.

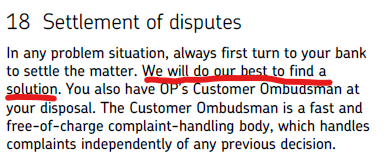

Can I objectively prove this is a racist case? I do not know. Probably not. Again, overcompliance technically fits here as well, since (repeating myself) I am from the risk group. But on the other hand, I did come forward beforehand, I did try to find a way forward, I was fine with temporary (and reasonable) restrictions to the money I was depositing. I was trying to find a solution along with OP, as per their own Section 18.

I do not know about you, whoever is reading this, but I do not think I fit the profile of a putinist, or a warmonger or any malicious actor. My actions show openness and readiness to discuss things. My transactions do not either. Considering how much push there is right now for the narrative that "immigrants are bad and causing problems" (including the issues discussed by Specialists in Finland) it is just… Very hard to think otherwise.

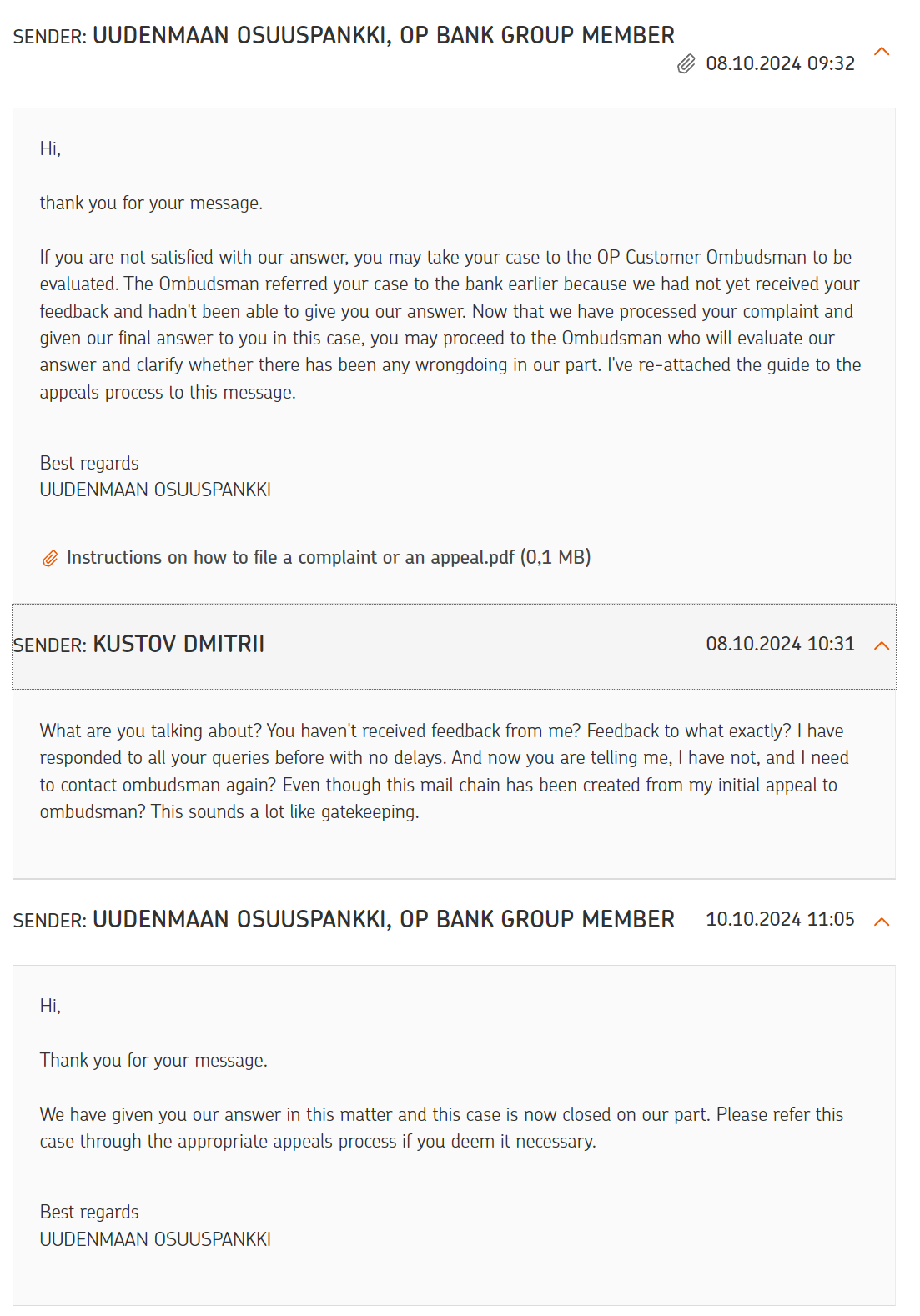

Will this post change anything? Again – I do not know, and probably not. I doubt OP will reach out to me to try to fix things (if they even see this). Although, I'd love this to happen, I would love to work with them to not only fix things for me, but to find a better way to fix this for everyone, for the system to be fair to other people, who are not native Finns, too. I doubt other banks are much better either, based on comments you can find for them. I do not doubt that some people will see this as me playing a victim and being "typical Russian" or something like that.

At least I know that now you have this detailed and evidence-based negative review of the bank. And a strong recommendation to stay away from Osuuspankki and probably OP group.